You may need to borrow money at the most unexpected time of your life and need it badly. The obvious solution is to go to the bank and get a loan. However, if your credit score and history aren’t ideal, you are unlikely to find a lender willing to lend your money easily or on good terms, if any. Luckily for you, title loan lenders care about something completely different.

Learn about title loan requirements and see whether you can qualify for a loan to finance your needs.

What Is a Car Title Loan?

Car title loans are short-term loans where the borrower’s car is used as collateral. Collateral is an asset (in this case, a vehicle) that a borrower provides as a guarantee of repaying the money. A lender can repossess the vehicle if a borrower fails to repay the money on time.

That’s why some leaders partnering with Titelo require proof of income, along with other documentation, to ensure this dire situation is avoided. At the same time, stable income may not be the decisive criterion for other lenders.

How to Get a Car Title Loan?

Titlelo has significantly simplified the process of getting a car title loan. You don’t have to visit any branch since everything can be completed from the comfort of your home.

Gathering all the documents may also be a stressful experience; therefore, having all the information gathered for you online will significantly speed up the process.

We offer you two means of getting a title loan: online and via the phone. There is an intuitive and short form you can fill out online with your information:

- Full name

- Telephone number

- Zip code

- Vehicle information

You may also choose to give us a call at 855-341-4500. The information we require is the same as on the form.

Note that a car title loan is legal in 23 states with limitations.

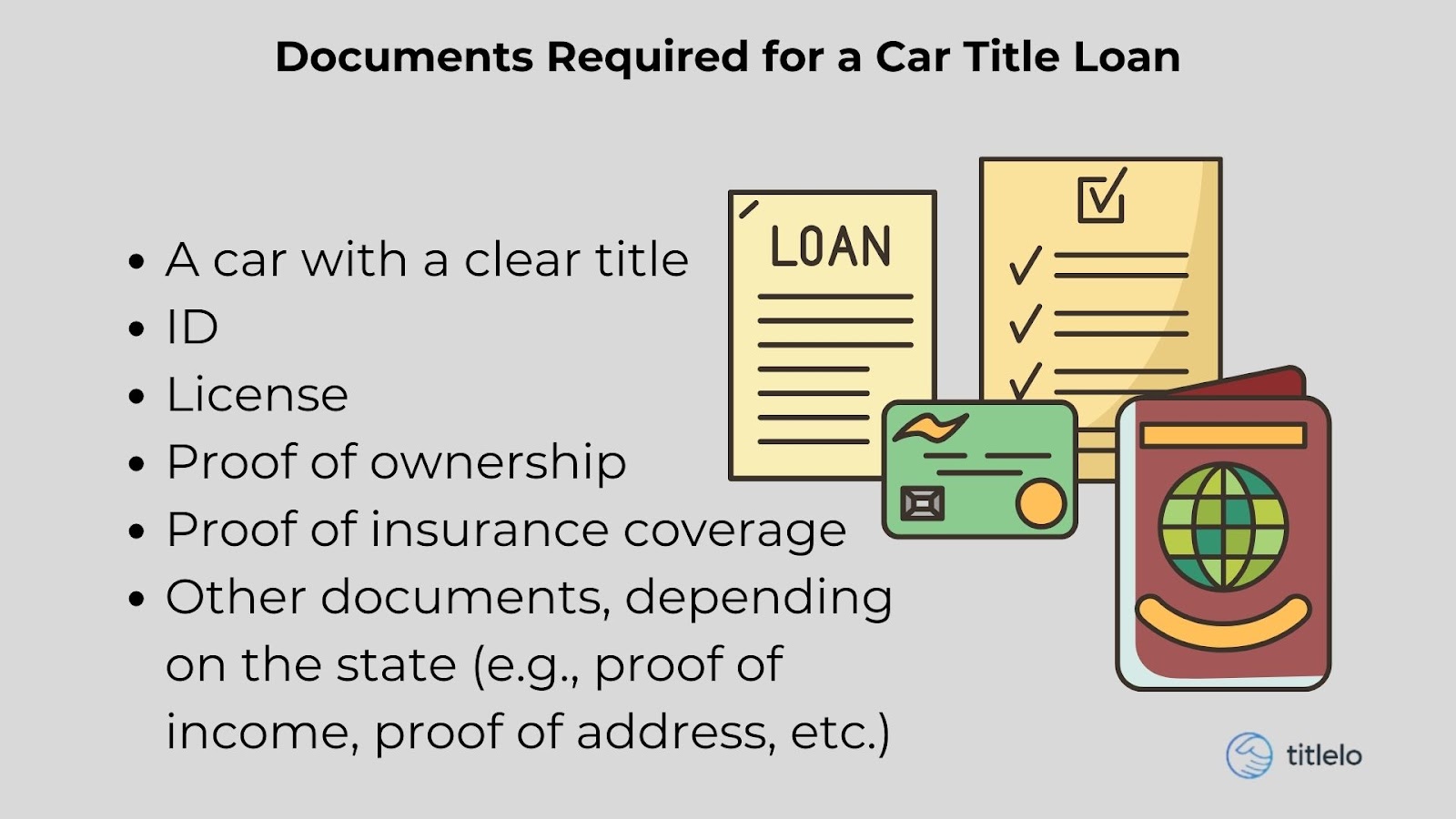

What Documents Do I Need for a Title Loan?

At Titlelo, there are two process stages: pre-approval and approval.

Here is the information you would need to provide us with for the pre-approval stage:

- Personal information (full name, contact details, zip code)

- Vehicle information (make, model, year, mileage)

Once you are qualified for a car title loan, our lenders will require a set of the following documents:

- ID (driver’s license, U.S. passport, government-issued ID)

- A lien-free title in your name

- Proof of income* (bank statement, pay stubs, social security, etc.)

- Other (proof of insurance, proof of address, or registration)

- The final set of required documents will depend on your state

*The requirement to provide proof of income will also depend on the lender. Some providers will lend money without you having a stable income, while it can be a decisive document for other lenders.

This set of documents will allow a lender to review your case and decide what amount of money you are eligible for. Applying online also means convenience and a speedy process for you without leaving your home.

Title Loan Requirements

Every lender and state has specific title loan requirements that qualify borrowers. A car title loan has a few, so most borrowers are eligible to apply and are approved.

To apply for a car title loan, you must:

- Be 18 or over

- Own a lien-free vehicle*

- Apply for a car title loan online

- Get approved for a loan

- Receive your money

*A lien-free car title does not hold any claims by another creditor. It is a crucial criterion for lenders to know that your car cannot be repossessed or seized by a third party.

Getting a car title loan does not mean our lenders confiscate your car and its keys. It is a common misconception. Instead, you get to keep your car and drive it.

If you have previously applied for a title loan with another company, you can still do that same with Titlelo. We will help you connect with your lender to refinance your current loan. As a result, you will be able to save money and get a new loan title with a lower interest rate.

Proof of Income

Technically, you do not have to be employed in order to be approved for a car title loan. Having no income source is usually considered high-risk credit, and our lending providers currently do not approve such borrowers.

Still, there should be some income in disability, child support, alimony, social security, self-employment, etc. You increase your chances of getting a car title loan by providing proof of one of the above.

How Do Car Title Loans Work?

The only criterion to get a car title loan is the ownership of a vehicle. To apply for a loan, your car should be lien-free. Only by having the required documents can you qualify for a loan.

To remind you, the required documents include the following:

If you fit the criteria, you will need to hand over your car title and only then receive the money. You will need to repay the money within 30 days of taking out a title loan. Like payday loans, you will pay a lump sum at the end of the term. The inability to do that on time will result in losing ownership of your vehicle.

Here is how to get a title loan in a few steps:

- Fill out the form.

- Get a call from one of the Titlelo representatives who will verify your information.

- Titlelo will connect you with one of the lenders who will:

- Inspect your vehicle

- Determine the range of loan amounts you can ask for

- Receive your funds in your bank account or as a check shortly after the approval.

- When the debt is due, repay it and receive your vehicle title back.

What Are Car Title Loan Fees and Interest Rates?

When taking out a title loan, our partnered lenders disclose potential fees or penalties you may be eligible to pay. Most of these fees are associated with early or late payments, as car title loans typically have a defined repayment term. Before finalizing the agreement, taking note of what you are not advised to do helps.

The interest rate will depend on your individual case. Although your credit history has no impact, your ability to pay for the taken loan may have a positive impact on the interest rate. Your financial ability to cover the cost of a loan may bring the interest rate down, depending on the lender, residency, and state regulations. On average, you can expect the interest rate to vary from 20% to 50%.

How Much Cash Can You Get with a Car Title Loan?

You can expect a loan that equals 25%- 50% of your vehicle’s value. A lender will examine your car title and the vehicle itself to determine its worth. The range of debt you can receive varies from the minimum loan amount of $200 to the maximum loan amount of $25,000 and more, although the average amount is $1,000.

Car Title Loan Example

Let’s say you need to borrow $3,000 for about a month. As the rules imply, you will need to pay the money within 30 days and the interest rate. The interest rates range from 25% to 50%. For this example, let’s assume the interest rate is 30%.

The additional fees come to $900, so the total amount is slightly below $4,000, precisely $3,900.

How Can I Repay My Car Title Loan?

When the money is in your account and the time has come to repay the loan, there are a few options to get your title back. Most of the repayment methods depend on the lender, and they include:

- Online payments

- Payments over the phone

- Direct deposit or money transfer

- Mailing a check

- Paying at the physical office

To reduce or eliminate the risk of losing your car title, make sure to do the following before taking out a loan:

- Borrow the amount you are sure you can repay

- Make your research and read through the terms and conditions

- Set a reminder to repay your loan on time (earlier or later payments may incur penalties)

- If you face financial difficulties and are unable to repay your car title loan on time, speak to your lender to find the best solution for both parties

Pros and Cons of Getting Car Title Loans

Whichever loan you decide to take out will have its benefits and drawbacks. A car title loan isn’t ideal and might not be suitable for your needs, but it is one of the quickest loans with a moderate risk level.

Pros of Getting a Car Title Loan

| Fast cash | Limited to no credit check | Speedy approval |

| In a few days, you can receive loan approval and funds as soon as possible. Some payment methods are instant (e.g., if you agree to accept a check), while others may take 2-3 working days to be transferred to your bank account. | We do not check your credit score during the pre-approving process. However, it can be required in some states. Nothing to worry about, even if your credit score isn’t high. The rating does not influence the lender’s decision. It may only help the lender decide on the amount you can borrow. | Pre-approvals at Titlelo are instant. This means you can immediately proceed to the next stage as soon as you provide all the required information. The loan approval takes up to 24 hours. The lenders take this time to verify the information provided by you, the condition of your vehicle, and to underwrite your loan. |

Cons of Getting a Car Title Loan

| Short repayment loan term | High fees and interest rates | You risk losing your vehicle |

| Although the repayment term varies from state to state, the loan is usually due within 30 days. The loan is generally paid at the end of the term, and there may be a prepayment penalty. However, Titlelo does its best to partner with loan providers that do not charge for preparing before the due date. | At Titlelo, you don’t pay loan-processing fees, and most lenders do not charge a prepayment penalty. However, the interest rate will be higher than that of traditional loan providers. Due to the title loan’s nature and its accessibility to borrowers with low credit scores, there may also be extra fees that will be discussed and disclosed before finalizing the agreement. | If you don’t pay off your debt, the lender will repossess your car and sell it. |

Conclusion

Getting a loan with a car title isn’t complicated and can be completed within the same day. The application process is divided into two stages: verification of your information and inspection of your vehicle. An auto title is a somewhat accessible loan as you don’t have to have a high credit score or a flawless credit history.

The most important criteria to take out a title loan are to have a working car, a clear title, and some source of income.

Titlelo will assist you and match you with the best lender in your area. Apply now and get approved within 24 hours!

Frequently Asked Questions

Are title loans illegal in Ohio?

A car title loan is legal in 23 states, excluding Ohio. Ohio has introduced a Short-Term Loan Act. In short, it is unlawful for lenders to possess a borrower’s title.

Other states where title loan is banned are Michigan, Arkansas, Rhode Island, Vermont, Wyoming, and others.

Are title loans legal in Virginia?

Car title loans can be applied for in 23 states, including Virginia, Louisiana, Missouri, Florida, and other states.

If you have an unexpected expense, it is legal to provide your car as collateral for the short term and pay for your medical bill, car repair, utility expenses, etc.

Can a car loan and title be under different names?

As a rule, the car title has to be in the name of a borrower. If your vehicle title has your name along with another one, it could be possible to take out a loan. However, the procedure may differ from state to state – therefore, we recommend you contact us on this matter.

If your car title has two names, a lender will likely ask for both names to be included on the application.

Do title loans affect credit?

Typically, your credit check isn’t the priority for car title lenders. And that is why taking out this loan won’t affect your credit.

Repaying the loan will not improve your credit score, either. However, if you default, your lender must abide by the law and report the case to the Fair Debt Collection Practices. This, in turn, will affect your credit score adversely. On the other hand, if you cannot pay off the debt, your car will be sold, and the amount received will cover the debt.

Chad is a seasoned executive with an impressive track record spanning over two decades in the Fintech sector across diverse technologies and financial industries. With a wealth of knowledge accumulated throughout his career in finance & technology, he is dedicated to ensuring that both our employees and clients benefit from the highest levels of expertise and an unwavering commitment to customer service. Chad’s forward-looking approach and exceptional leadership skills have played a pivotal role in the success of his businesses, empowering consumers to proactively navigate the ever-evolving challenges of everyday life. When he’s not charting new horizons in the business world, Chad enjoys quality time outdoors with his wife and kids, as long as the Texas weather doesn’t hit a scorching 110 degrees! 😉